Getting kids to be financially aware is a struggle. While many high street banks will offer junior accounts, they don't offer you a lot of control. In fact, they're mostly just a gateway to an adult account some years down the line.

Revolut Junior is a little different, because the account that you setup for your child or children (aged 7-17) is linked to your own Revolut account. That means it comes with many of the benefits that Revolut brings its regular customers, like instant notifications about spending. Yes, you'll be able to see where your child is spending, in real time through your own Revolut app.

You have to have a Revolut account yourself to setup a Junior account (and it's only open to Premium and Metal customers, i.e., the paid-for adult accounts), and you'll control it through your main account.

That extends to the Revolut Junior account not working at age-restricted retailers, as well as custom controls so you can decide exactly how they can spend their money. In the future, there will also be added features, like payment for chores and savings targets.

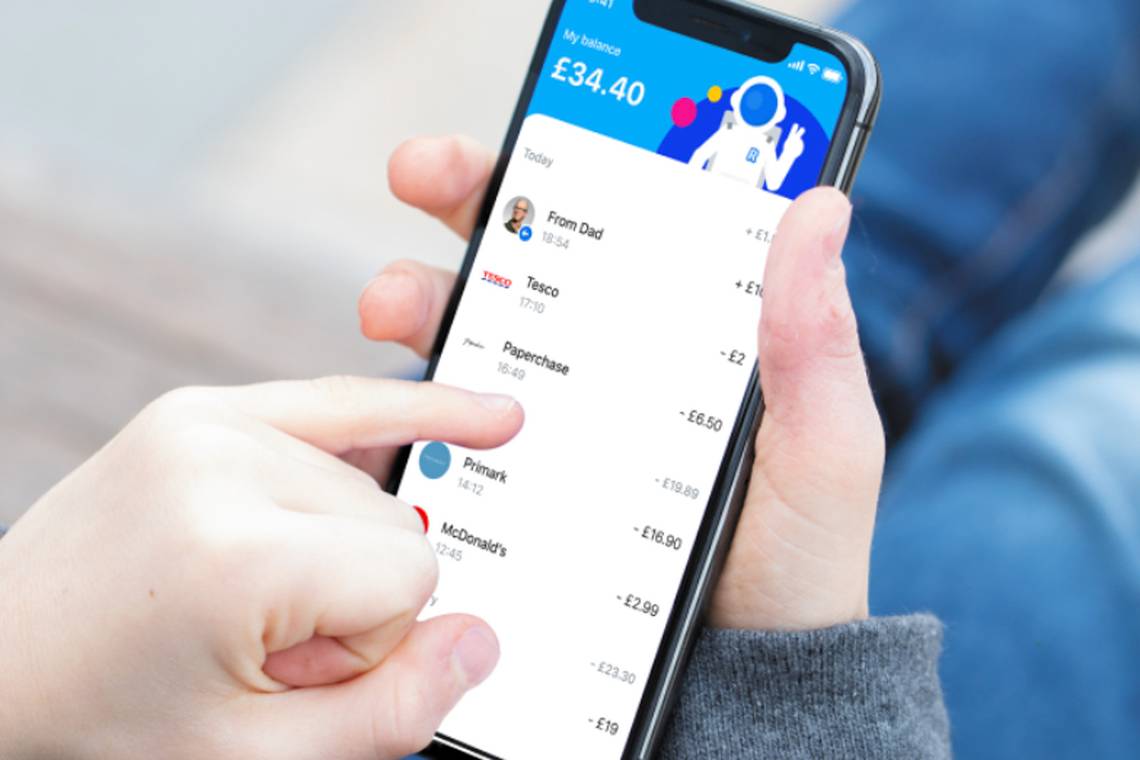

There's an app designed specifically for kids and this will have all the breakdowns of spending that Revolut offers its other customers, meaning you can see in real time exactly how much money you have and where you've been spending it. The card number is also printed on the back of the card rather than the front, designed to stop them accidentally sharing it online when boasting about having a card.

The kid's app isn't essential, if they don't have a smartphone, they can just use the card as normal for spending, with the parent's app still getting all the information.

It's worth noting that Revolut works as a prepay card, so rather than this being a full current account, the parent will have to transfer money over to the child's card from their own Revolut account. That's not going to help if a teenager has a job that pays by bank transfer and it also means there's no high street bank to walk into to deposit birthday money or cheques.

But for the parent it means that things like pocket money can be paid straight into the card for the child to have access to - with the option of online or offline spending with that card (with all permissions staying with the parent).

It's certainly an interesting and simple way of introducing children to spending with a card and of course, once the card has run out of funds, there's no way they can spend more than they've got.